![]()

Introduction

In recent years, the world of cryptocurrency and Non-fungible tokens (NFTs) has experienced explosive growth. NFTs, which represent unique digital assets like artwork, collectibles, and virtual real estate, have gained widespread attention and become a significant part of the crypto ecosystem. However, with the increasing popularity of NFTs, it’s essential for both creators and collectors to understand the tax implications associated with these digital assets. In this blog post, we will explore the basics of reporting NFTs on taxes and provide guidance on navigating crypto taxation wisely.

Understanding NFTs

Before we dive into the taxation aspect, let’s briefly review what NFTs are. Non-fungible tokens (NFTs) are tokens that are based on blockchain technology and serve as a representation of ownership for a particular digital item or content. Also, unlike cryptocurrencies like Bitcoin or Ethereum, which are fungible and interchangeable, NFTs are non-fungible, meaning each token is unique and cannot be exchanged on a one-to-one basis with another NFT.

NFTs can encompass various digital assets, including digital art, music, virtual real estate, in-game items, and more. They are bought and sold on various online marketplaces. Also, often using cryptocurrencies such as Ethereum.

Taxation of NFTs

The taxation of NFTs is a complex and evolving area, and it varies from country to country. Here are some essential points to consider when reporting NFTs on your taxes:

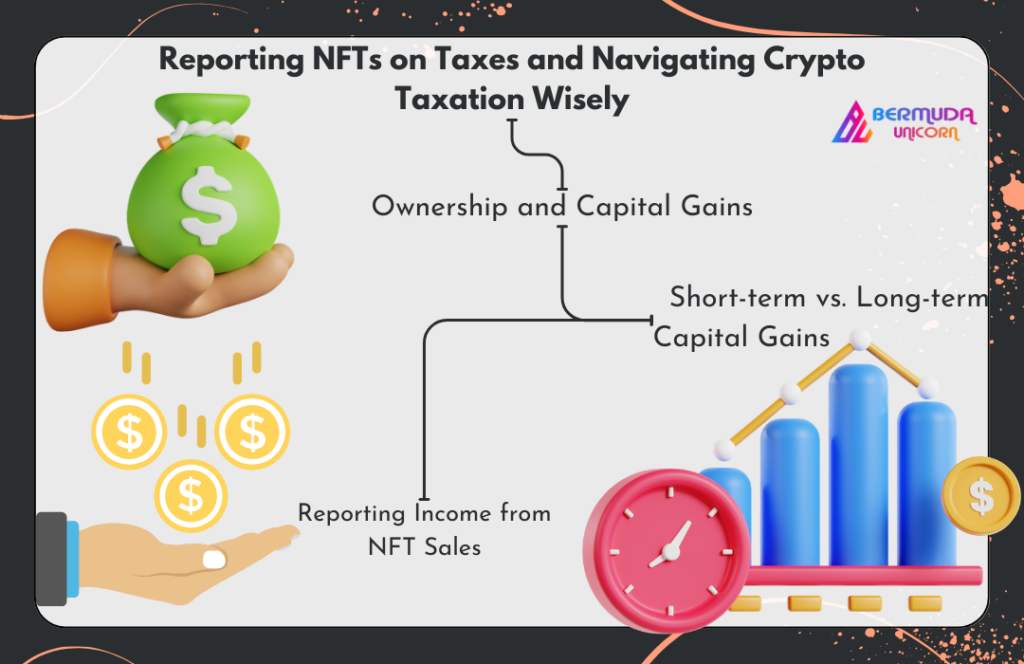

1. Ownership and Capital Gains:

In many jurisdictions, NFTs are treated as property for tax purposes. When you purchase an NFT, it’s akin to acquiring a piece of property. Any increase in the NFT’s value from the time of acquisition to the time of sale may be subject to capital gains tax. Keep detailed records of your NFT transactions, including purchase prices and dates, to calculate capital gains accurately.

2. Short-term vs. Long-term Capital Gains:

Tax rates on capital gains can differ depending on whether the NFT was held for a short or long duration. Short-term capital gains are usually taxed at higher rates than long-term gains. The definition of short-term and long-term holding periods varies by country, so consult your local tax regulations.

3. Reporting Income from NFT Sales:

If you sell an NFT and make a profit, the profit may need to be reported as taxable income. Ensure you keep records of all your NFT sales and accurately report them on your tax return.

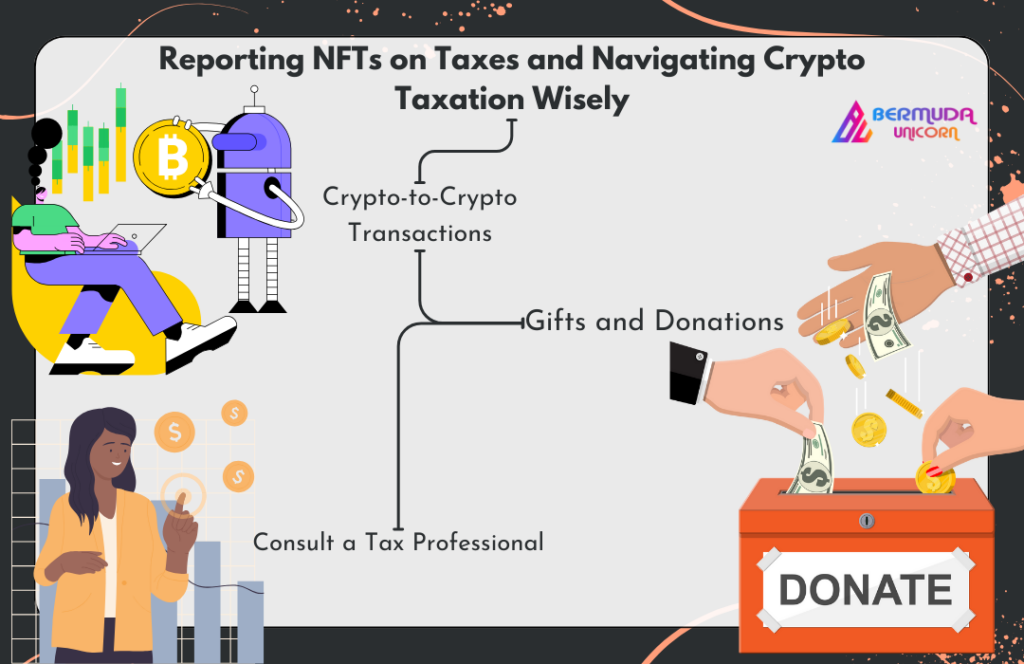

4. Crypto-to-Crypto Transactions:

If you use cryptocurrencies to purchase NFTs, these transactions may also have tax consequences. For instance, trading Ethereum for an NFT is a taxable event in some jurisdictions, and you may be required to calculate and report any capital gains or losses.

5. Gifts and Donations:

If you gift or donate an NFT, there can also be tax implications. Gifting an NFT may trigger gift tax reporting requirements, while donating an NFT to a qualified charity may entitle you to a tax deduction.

6. Consult a Tax Professional:

Given the complexity of crypto taxation, it’s highly advisable to consult a tax professional or accountant with expertise in cryptocurrency when preparing your tax returns. They can provide guidance specific to your situation and help you maximize tax benefits while staying compliant with the law.

Conclusion

Navigating the taxation of NFTs can be a challenging task, given the evolving nature of cryptocurrency regulations and the uniqueness of these digital assets. However, it’s crucial to stay informed and compliant with tax laws to avoid potential penalties or legal issues down the road.

Remember to keep meticulous records of your NFT transactions, including purchase and sale prices, dates, and any associated fees. Consult with a tax professional to ensure you report your NFT-related income and capital gains accurately.

As the world of cryptocurrencies and NFTs continues to evolve, staying informed and proactive about tax matters is essential to make the most of your digital asset investments while maintaining financial transparency and integrity.

Frequently Asked Questions (FAQs)

1. Are NFTs subject to taxation?

– Yes, in many countries, NFTs are subject to taxation. They are often treated as property for tax purposes, and transactions involving NFTs may trigger capital gains taxes.

2. How do I calculate capital gains on NFTs?

– Capital gains on NFTs are typically calculated as the difference between the selling price and the purchase price. Short-term gains (held for a short period) may have different tax rates than long-term gains (held for a longer period).

3. Do I need to report every NFT transaction?

– Yes, it’s essential to report all NFT transactions, including purchases and sales, on your tax return. Keeping detailed records of these transactions is crucial for accurate reporting.

4. Can I offset NFT losses against gains?

– In many jurisdictions, you can offset NFT capital losses against capital gains. This can potentially reduce your overall tax liability.

5. What if I received an NFT as a gift?

– Receiving an NFT as a gift may have gift tax implications, depending on your country’s tax laws. Consult with a tax professional for guidance on reporting such transactions.